Here is something that does not happen often in Indian equities: a company grows revenue at 33% year-on-year, expands its order book to ₹8,366 crore, enters semiconductor packaging, signs satellite technology JVs, and participates in India's biggest electronics manufacturing opportunity in a generation — and still watches its stock fall 60% from its peak.

Kaynes Technology is that company. And the story of why its shares crashed despite strong headline growth is, in many ways, the most instructive case study in Indian mid-cap investing right now.

THE NUMBERS: GOOD HEADLINE, TROUBLED DETAIL

For FY26, Kaynes Technology reported consolidated revenue of ₹3,626 crore — growing 33.2% year-on-year from ₹2,723 crore. EBITDA grew 39.8% to ₹574 crore. Profit after tax increased 24% to ₹364 crore. The order book expanded to ₹8,366 crore from ₹6,597 crore the previous year — providing roughly two years of revenue visibility.

Taken in isolation, these numbers would typically indicate a healthy, growing business. The market's reaction — a 60% decline from the 52-week high — reflects something more fundamental than a bad quarter.

At the start of FY26, management guided for revenue of ₹4,500 crore. This was subsequently cut to ₹4,000 crore. Actual revenue came in at ₹3,626 crore — nearly 20% below the original guidance and still ₹374 crore short of the revised, lower target.

In Q4 specifically, management had indicated quarterly revenue could reach around ₹1,700 crore. Actual Q4 revenue came in at ₹1,243 crore. Net profit in that quarter fell 21.5% year-on-year from ₹116 crore to ₹91 crore. PAT margins compressed from 11.8% to 7.3%.

The pattern — guidance cuts followed by further misses on the lowered expectations — is what eroded investor confidence more severely than any single weak number could have.

THE CREDIBILITY PROBLEM: WHAT ACTUALLY WENT WRONG

Kaynes missed its guidance for a specific, traceable set of reasons — not structural business deterioration, but execution gaps in two particular areas.

The first was a sharp revenue collapse from a major electric vehicle customer, where Kaynes served as the sole supplier. Revenue from that customer fell approximately 90% in FY26. Management attributed this to the customer's own production slowdown rather than any loss of business — but the magnitude of the impact, and the fact that it wasn't adequately signalled to investors until late in the year, raised questions about demand forecasting and commercial concentration risk.

The second was smart meter installation delays. The government's Revamped Distribution Sector Scheme has sanctioned 20.33 crore smart meters — but only 4.69 crore had been installed as of March 2026, representing just 23% of the target. Kaynes, which had taken on AMISP-type contracts that require it to carry the full installation burden rather than simply supplying meters, found itself with ₹1,365 crore of metering-related receivables against only ₹971 crore in metering revenue for the full year. The mismatch between revenue recognised and cash actually collected turned operating cash flow negative by ₹600 crore for FY26.

An investor on the Q4 earnings call asked a pointed question: why did management hold its guidance 75 days into the quarter when the final result would be so far below expectations? Management acknowledged that samples had been approved, materials ordered, and pre-manufacturing started — but that a key order was delayed rather than cancelled. That distinction — delayed, not lost — matters for the long-term thesis. But it doesn't fully address the communication gap.

THE CASH FLOW PROBLEM: WHEN PROFITS DON'T BECOME CASH

The most concerning metric in Kaynes' FY26 results is not the revenue miss or the margin compression. It is the working capital trajectory.

Net working capital days increased from 87 in FY25 to 125 in FY26. Receivable days rose from 84 to 134 — meaning Kaynes waits an average of 4.5 months to collect what it is owed. Inventory days moved up from 91 to 97.

Cumulatively, over the eight years since FY18, Kaynes has reported positive PAT in most years — cumulative profits of ₹1,006 crore. But cumulative operating cash flow is negative ₹568 crore. Profits have consistently not converted into cash at the same pace they have been reported.

This divergence between accounting profit and cash generation is not unusual for a rapidly growing manufacturing company — capital is needed for working capital before revenue fully converts. But at 125 working capital days on a ₹3,626 crore revenue base, the cash tied up in operations is significant and growing. It limits the company's ability to self-fund its expansion without repeated recourse to debt or equity markets.

Management has indicated it intends to shift the smart meter business model away from full AMISP contracts toward simply supplying meters as products — which would dramatically improve the cash conversion cycle. But management itself acknowledged that approximately 50% of FY27 metering revenue could still come from the old model. The transition will take time.

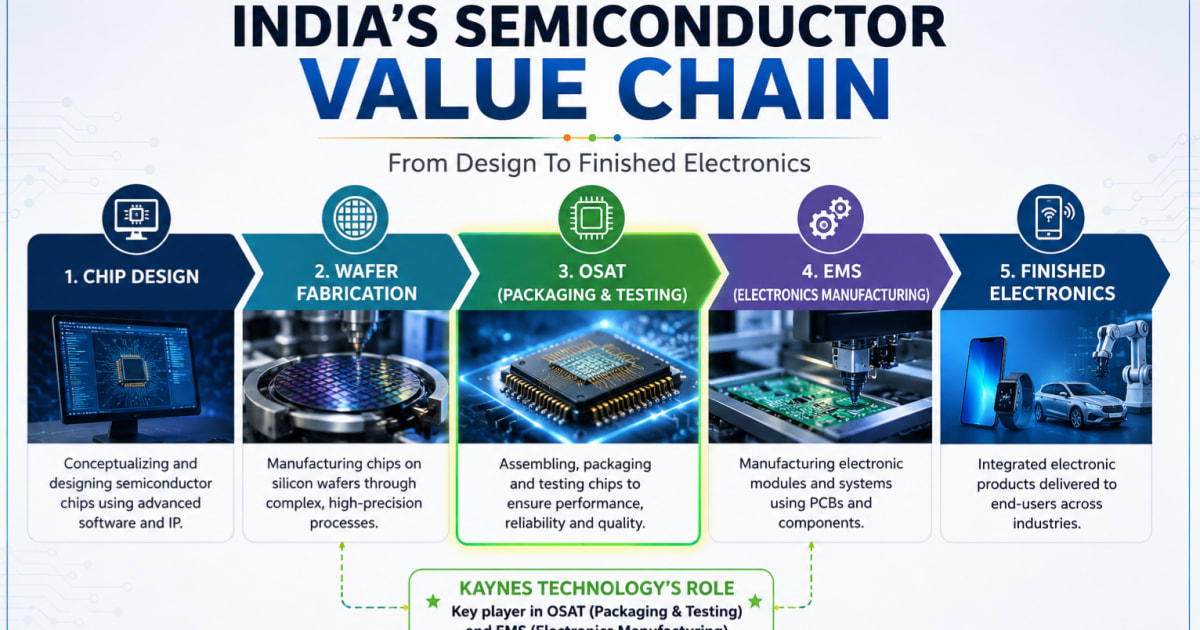

THE SEMICONDUCTOR BET: KAYNES' MOST AMBITIOUS EXPANSION

Despite all the near-term execution pressures, Kaynes is simultaneously making the boldest strategic move in its history: entering semiconductor OSAT — Outsourced Semiconductor Assembly and Testing.

The company's gross block increased from approximately ₹790 crore in FY25 to ₹1,791 crore in FY26 — more than doubling in a single year — as it scaled up semiconductor packaging infrastructure alongside its existing EMS facilities. Kaynes Semicon has also reached a final agreement with SEALSQ, the Swiss post-quantum cryptography company, to develop a sovereign Indian post-quantum semiconductor joint venture in alignment with MEITY. A Japan technology partnership for semiconductor capability building has also been announced.

The ISM 2.0 framework — India's enhanced semiconductor mission recently approved with ₹1.25 lakh crore in Finance Ministry backing — provides the policy context for Kaynes' semiconductor ambitions. CG Power, Kaynes, and MosChip all rallied on the ISM 2.0 announcement, reflecting market recognition that the policy environment for domestic chip packaging is more supportive now than at any point in India's history.

On the PCB front — Kaynes is building High Density Interconnect printed circuit board manufacturing capacity, which gives it backward integration into a component currently almost entirely imported. PCBs are the substrate on which virtually every electronic device is built, and India's import dependence in this category has been a persistent vulnerability for the domestic EMS sector. A domestic HDI PCB capability meaningfully improves Kaynes' value chain positioning.

The tension the market is wrestling with is straightforward: these investments are correct and strategically important, but they are capital-intensive upfront and revenue-generative only over a 2-4 year horizon. The company is simultaneously absorbing the cost of its future while trying to deliver on its present commitments — and the present has disappointed enough times that investors are demanding visible evidence of the former before crediting the latter.

THE GOVERNANCE QUESTION: DECEMBER 2025

No complete account of Kaynes' correction can omit the December 2025 episode. Questions surfaced about related-party disclosures involving Kaynes and its associates. The stock lost nearly ₹10,000 crore in market value over three trading sessions. The former MD subsequently reached a SEBI settlement, with a payment of ₹23.43 lakh confirmed in the secretarial compliance report for FY26.

When a company growing at 33% annually and building semiconductor capacity loses ₹10,000 crore in market value over disclosure questions, it tells you how thin the tolerance for governance ambiguity is at the premium multiples that high-growth EMS companies commanded. The SEBI settlement provides some resolution, but the episode left a residue of caution in institutional portfolios that has contributed to the valuation derating.

Separately, Independent Director Heinz Franz Moitzi resigned effective May 31, 2026, citing personal and professional commitments. Board composition changes at a company already under scrutiny add to investor wariness, even when each individual development has a plausible non-governance explanation.

THE CORE BUSINESS: STILL GENUINELY STRONG

The risk in all of this analysis is losing sight of what Kaynes actually built, and why it attracted premium valuations in the first place.

Revenue has grown at a 46% CAGR since FY20, from ₹368 crore to ₹3,626 crore in FY26. Profit after tax grew from ₹9 crore to ₹364 crore over the same period. The end markets — industrial electronics, automotive and EV, railways, aerospace, defence, medical devices, and smart infrastructure — are among the highest-growth segments in India's manufacturing landscape. Jefferies expects Indian EMS companies to deliver 44% EPS CAGR between FY25 and FY28 on execution.

The order book at ₹8,366 crore provides two years of revenue visibility. The company's presence in defence and aerospace — higher margin, stickier, and less commodity-like than consumer electronics EMS — has been growing. Management has targeted increasing new product development and value-added solutions to approximately 30% of revenue, which would move Kaynes toward a more design-led, product-led model rather than pure assembly services.

The core EMS business, stripped of the smart meter complexity, shows improving working capital — management noted that core EMS working capital days improved from 83 in FY24 to 53 in FY26, a meaningful improvement hidden by the metering business's impact on consolidated numbers.

THE VALUATION: HAS THE CORRECTION CREATED OPPORTUNITY?

At its peak, Kaynes traded at a price-to-earnings ratio above 100x — a multiple appropriate only for companies growing earnings at 50%+ annually with pristine execution. The current market capitalisation of approximately ₹22,500 crore implies a forward PE of roughly 55-60x on FY27 consensus estimates — still above the broader market and most manufacturing peers, but meaningfully below the peak.

The question every investor is now asking is whether the 60% correction has adequately repriced execution risk, or whether the combination of guidance credibility issues, working capital strain, negative operating cash flow, and governance questions warrants a further discount before the stock becomes genuinely attractive.

Three specific catalysts could restore confidence. First, EBITDA margins expanding sustainably above 15% — proof that the business generates operating leverage as it scales. Second, a visible order book increase in high-margin defence and aerospace segments. Third, working capital days declining consistently as the smart meter business model transitions away from AMISP contracts.

Analysts at J.P. Morgan expect 20-25% revenue growth in Indian EMS over FY26-28, and count Kaynes among names they see delivering on this. Jefferies specifically prefers Kaynes and Syrma SGS over Dixon Technology, citing the PLI's focus on components over finished goods assembly.

THE HONEST ASSESSMENT

Kaynes Technology is not a broken business. It is a promising business carrying a higher burden of proof than most investors originally expected, created by a combination of execution gaps, a difficult government customer, governance questions, and the market's natural intolerance for premium-valued companies that miss guidance.

The semiconductor and PCB investments are strategically correct. The end markets are genuine. The order book is real. But the market is no longer willing to pay for potential on faith alone — it wants quarters of execution that demonstrate the new capacity is generating margin-accretive revenue, that working capital is improving, and that management's visibility into its own business has become more reliable than it appeared in FY26.

Value Research summarised it clearly: "a promising business carrying a higher burden of proof than most investors signed up for." That burden must now be discharged through results, not guidance.